Valuation is not an exact science by definition, and this becomes even more apparent when valuing startups. Startups typically have negative cash flows that are expanding, minimal or no past financial data and projections, and frequently no proof of concept. Therefore, traditional approaches such as the income approach, the market approach, and the net assets approach, which are used to determine the start-up business value/the EV, are ineffective because start-ups and the majority of early-stage companies lack the required financial performance indicators.

Valuation of a startup presents a number of obstacles, necessitating a variety of approaches from possible investors. Due to the absence or scarcity of historical data and the uncertainty of forecasts, qualitative factors play a crucial influence. Hence, factors such as management experience, first customers and revenue, a clearly defined target market, or a minimum viable product (MVP) should be included in the valuation process.

As a startup founder, it is critical for you to understand a precise range of how your startup can be valued, especially if you are considering selling it.

Valuation techniques for new businesses

We can find six main strategies that are frequently utilized in practice and applied to various stages of a startup. The list is endless, and valuation professionals frequently employ a combination of the approaches shown in the table below.

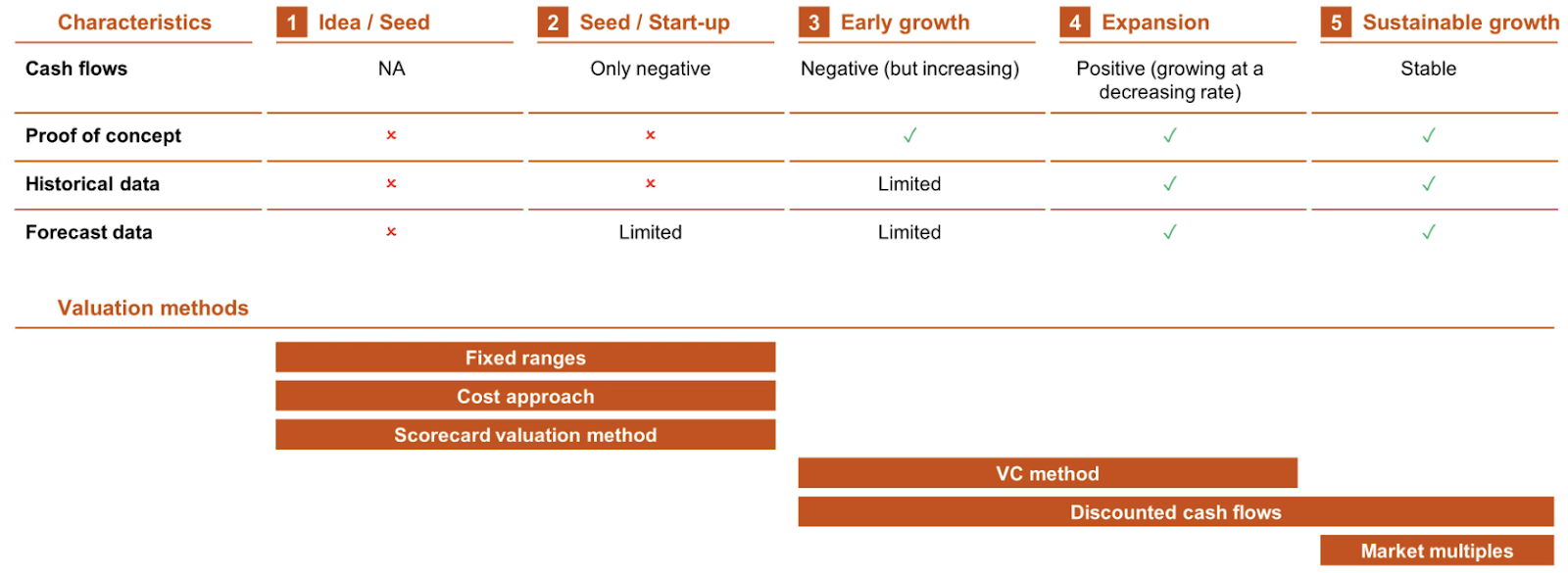

The chosen method of valuation relies on the level of maturity of the target entity:

Source: https://www.pwc.com

Methodology for Early Stage (Idea and Seed) startups

The valuation procedures for early-stage enterprises would differ from those used for mature companies. As shown in the preceding table, the fixed ranges technique, the cost approach, and the scorecard valuation method may be utilized for the valuation of enterprises at the Idea/Seed and Seed/Start-up stages. With the fixed ranges method, incubators propose a 'take or leave' investment based on the set ranges of capital supplied in exchange for an equity stake. The cost approach assumes that an investor is willing to cover the expenses already incurred by the target organization to reach its current level. In order to analyze the worth of the target company using the scorecard technique, potential investors have a list of evaluation criteria against which the target entity and its competitors are compared.

Methodology for Growth and Expansion Stages startups

The venture capital (VC) and discounted cash flows (DCF) approaches may be utilized to value companies in the Early Growth and Expansion stages. Using the VC technique, the startup’s value is evaluated based on its value in a few years (the so-called "exit-value"). This estimated future value is then discounted using a discount rate to get its present value. The DCF approach is utilized for organizations whose cash flows can be estimated with reasonable accuracy. DCF is a method for estimating the value of a target organization based on its anticipated future free cash flows. Then, these cash flows are discounted to their current value using a suitable discount rate, which is the weighted average cost of capital (WACC).

Methodology for Sustainable Growth Stages startups

Lastly, organizations that have entered the Sustainable Growth phase may be appraised using the DCF or market multiples methodologies. By employing the market multiples method, potential investors may take into account either the current market price of publicly traded peers or comparable transactions with disclosed multiples. Enterprise value-to-revenue (EV/R), enterprise value-to-EBITDA (EV/EBITDA), enterprise value-to-EBIT (EV/EBIT), and enterprise value-to-free cash flows (EV/FCF) are the most often utilized multiples in start-up valuation.

Use of the VC technique

For the valuation of a startup using the VC approach, the anticipated exit value was evaluated first. At the time of exiting the investment, the value was estimated as the predicted earnings multiplied by an industry-average income multiplier. Taking into account the predicted exit value, the start-up value at the valuation date was determined by applying the set discount rate to the exit value and the value at the valuation date. It is essential to highlight that the discount rate to be utilized in a start-up valuation is estimated in a manner distinct from the conventional method.

Use of the scorecard approach for valuation

A questionnaire is a complementary method of conducting a qualitative evaluation of a startup. For instance, when a startup has already reached the second stage but still exhibits characteristics of a Seed startup, including limited or missing historical financial data, ongoing product/service development, and negative cash flows.

Under the scorecard valuation approach, prospective investors are given a list of criteria against which the startup and its competitors are evaluated and scored in a binary manner. All of the aforementioned questionnaire's questions can be classified into two categories:

a) the management and services/products of the business; and

b) the market and business strategy of the company.

Each response are assigned a score; therefore, the higher the score, the greater the value of the startup.

Using the estimated weighted value from the questionnaire, the precise discount rate from the initial discount rate range can be computed based on the specified formula. Using the following formula:

Estimated discount rate = minimum value from discount rate range + (highest value from discount rate range - minimum value from discount rate range) * (100% - proportional part of the estimated value from the questionnaire).

As stated previously, valuation is not a precise science. Conventional methodologies such as the income approach, market approach, and net assets approach are not always suitable for valuing start-ups, as they are new businesses with minimal or no financial history. Other methodologies, such as the VC or scorecard methods, may be more suitable for evaluating startups. Yet, such methodologies necessitate a thorough comprehension of the market, the company being valued, and the valuation process itself.

.png)

.jpg)

.jpg)